Reassessing the Assessor’s Funding

Problematic formula fuels large surpluses at the expense of other public entities that levy property taxes

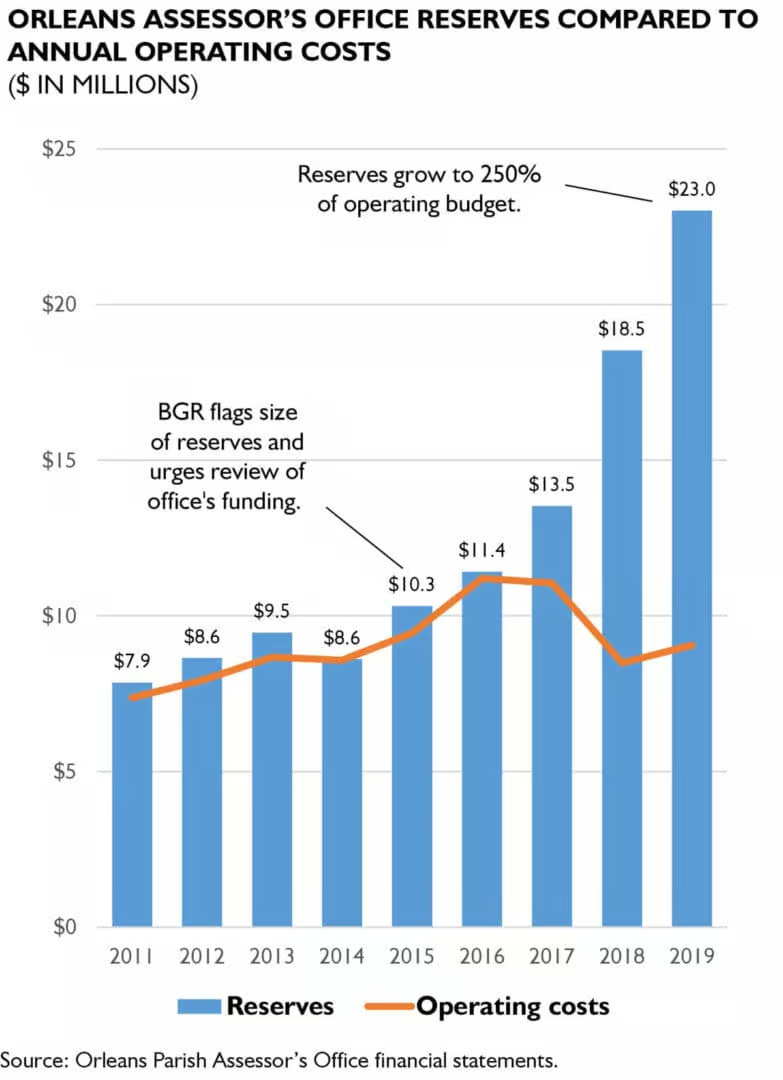

The economic fallout from the ongoing public health crisis has left the City of New Orleans, NOLA Public Schools and other local taxing bodies grappling with significant funding shortfalls. By contrast, the Orleans Parish Assessor’s Office anticipates its 2020 tax revenues will increase by $1 million (about 8%) to $13 million. Moreover, the assessor has accumulated $23 million in reserves, which is more than two-and-a-half times the office’s annual operating costs. These sizable reserves are linked to a problematic funding formula that BGR has urged policymakers to reevaluate.

Based on a State-mandated formula unique to Orleans Parish, the assessor’s office receives a fee equal to 2% of the total amount of property taxes billed each year. The fee will generate 96% of the office’s total revenue this year. As the parish tax collector, the City deducts the assessor’s fee, along with its own fee equal to 2% of taxes collected, from tax payments before distributing the net revenue to property tax recipients. The assessor’s fee will reduce this year’s estimated tax receipts for the four largest property tax recipients by the following amounts: the City ($5.6 million), NOLA Public Schools ($3.6 million), the Sewerage & Water Board ($1.3 million) and the Orleans Levee District ($870,000).

BGR has raised concerns about the assessor’s funding mechanism because the fee is not based on the office’s workload or expenditures. Rather, the fee grows along with increases in millage rates and property valuations. For example, a 2.5-mill tax that voters approved a few years ago for fire protection increased the assessor’s funding by about $200,000 per year, even though the office’s workload did not change as a result of the new tax.

Other assessors’ offices in Louisiana are funded either by a dedicated millage or by a legislatively-determined amount paid by all taxing entities on a pro-rata basis. A dedicated millage differs in two key ways from the fixed percentage of billed property taxes that the Orleans assessor receives. First, a millage is subject to rollback requirements when property valuations increase. Second, unlike a fixed percentage, a millage does not generate additional revenue when other entities impose new property taxes. Both characteristics could help control growth in the assessor’s reserves.

Since BGR first flagged the size of the assessor’s reserves in a 2015 report , the reserves have more than doubled as shown in the chart. The pace of growth has accelerated in recent years, with increases of $5 million and $4.5 million in 2018 and 2019, respectively. Based on information the assessor provided BGR, the office projects minimal growth in reserves this year. This is because the assessor plans to provide the City $3 million toward the purchase of a new revenue collection system. Absent this allocation, the assessor’s reserves would grow by a projected $3 million. The assessor says the new system will not only help the City, but also benefit the office by providing updated information on businesses, personal business property and occupational licenses.

After BGR called for a review of the funding formula, the assessor refunded $2.2 million of the office’s surplus revenue to the City in 2016. The City then distributed the revenue to local property tax recipients on a pro-rata basis. The assessor, however, has not made any refunds since then. Such refunds of excess revenue are at the assessor’s sole discretion. If the assessor refunded the $4.5 million in surplus revenue from 2019, the largest property tax recipients could expect to receive the following amounts: the City ($2 million), NOLA Public Schools ($1.3 million), the Sewerage & Water Board ($450,000) and the Orleans Levee District ($305,000).

Of the office’s $23 million in reserves, the assessor has set aside $10 million for new office space. The assessor says the office has outgrown its space at City Hall. State law requires the City to provide the assessor with a “suitable building.” The assessor says he has requested more office space, but the City has not provided it.

The assessor is in discussions with the judges of Orleans Parish Civil District Court about a joint facility that would also house the Clerk of Civil District Court, the Orleans Parish Sheriff’s civil division and the judges, clerk and constable of First City Court. The parties recently began exploring a potential renovation of the City-owned former Veterans Affairs hospital site. The judges do not yet have an estimate of what such a renovation would cost. They also continue to consider renovating their existing courthouse adjacent to City Hall. A 2016 feasibility study estimated this could cost roughly $65 million, although this amount would depend on the ultimate scope of the project.

A fund to build a new courthouse or to renovate an existing site contains about $11.6 million from a special document filing fee collected by the civil clerk’s office. The fee generates about $1.5 million a year. The fund would be in addition to any contribution from the $10 million the assessor has set aside. The judges said they are in discussions with the City to potentially issue bonds to finance a renovation, with the building’s occupants paying off the bonds.

The civil clerk’s office has $25.7 million in reserves, or about 175% of its operating budget. However, the clerk’s budget assigns all of the reserves to various purposes and projects. This includes $17.4 million set aside to cover accrued post-employment benefits, such as pensions and health insurance, in case future revenues are insufficient to cover these costs. The office is not required to maintain these reserves. This is a belt-and-suspenders budgetary approach that few government entities could afford. For example, the City would have to set aside more than $1 billion to cover its accrued post-employment benefits. The clerk’s office told BGR that it is in the process of evaluating the extent of any future contributions that it might make to the courthouse project above the statutorily-required special filing fee. The factors the clerk will consider include, among other things, the cost of the project, the size of the space allocated to the clerk’s office, the level of contributions by other occupants and whether the court entities could relocate to a potential new City Hall.

“The excess funding that the assessor’s office has set aside for new office space is revenue that would otherwise have gone to property tax recipients, many of which are struggling financially.”

The potential renovation is in the early stages and BGR has not taken a position on its merits. However, the problematic funding formula for the assessor’s office raises questions about its participation in the project. The excess funding that the assessor’s office has set aside for new office space is revenue that would otherwise have gone to property tax recipients, many of which are struggling financially. A refund from the assessor’s reserves could help these entities deal with the crisis. Because of this, the assessor should demonstrate that the new office space is a top community priority before participating. If the project does eventually move forward with the assessor’s participation, any contribution by the assessor should take into account the portion of the office space the assessor would utilize. Based on space estimates the judges provided BGR, the assessor’s office would occupy less than 10% of a joint facility.

Going forward, as BGR recommended in Assessing the Assessor, State and local policymakers should review the assessor’s unusual funding mechanism to better align it with the office’s needs. Given the excess revenue generated by the assessor’s fee, such a review is essential to ensure the efficient use of limited public resources. This is particularly important as the City, NOLA Public Schools, the Sewerage & Water Board and other local taxing bodies face revenue shortfalls related to the public health crisis or seek additional revenue to address high-priority needs.