Key Findings

During the past eight years, the single assessor has made progress in some areas important to implementing a model assessment system in New Orleans. The assessor has created an in-house data collection and maintenance program and linked the data to the City’s mapping technology. These steps have improved the accuracy of information used in determining property valuations. In addition, the assessor created a standard appeal process for property owners who want to contest their property valuations. The office has also strengthened the administration of property tax exemptions by strictly interpreting exemption criteria, regularly inspecting exempt properties and sharing more information with the public about exemptions and exempt properties. Finally, the assessor has enhanced the office’s website by making property records, maps, forms and other assessment-related data publicly accessible. The assessor’s progress in these areas is an accomplishment given the disjointed system and practices the office inherited from the seven-assessor system.

However, the single assessor has made insufficient progress in some fundamental areas.

BGR found that the assessor does not openly share with the public how the office uses mass appraisal technology to determine property values. Mass appraisal is the standard method for property valuation, using data and models to value large groups of properties at once while still adhering to appraisal principles. For this report, BGR asked the assessor for a demonstration of the office’s mass appraisal technology. The assessor denied BGR’s request. This lack of transparency deprives the public of a full understanding of how the office uses mass appraisal technology to value property. It also calls into question whether the assessor is using the technology properly and consistently to value property throughout the parish.

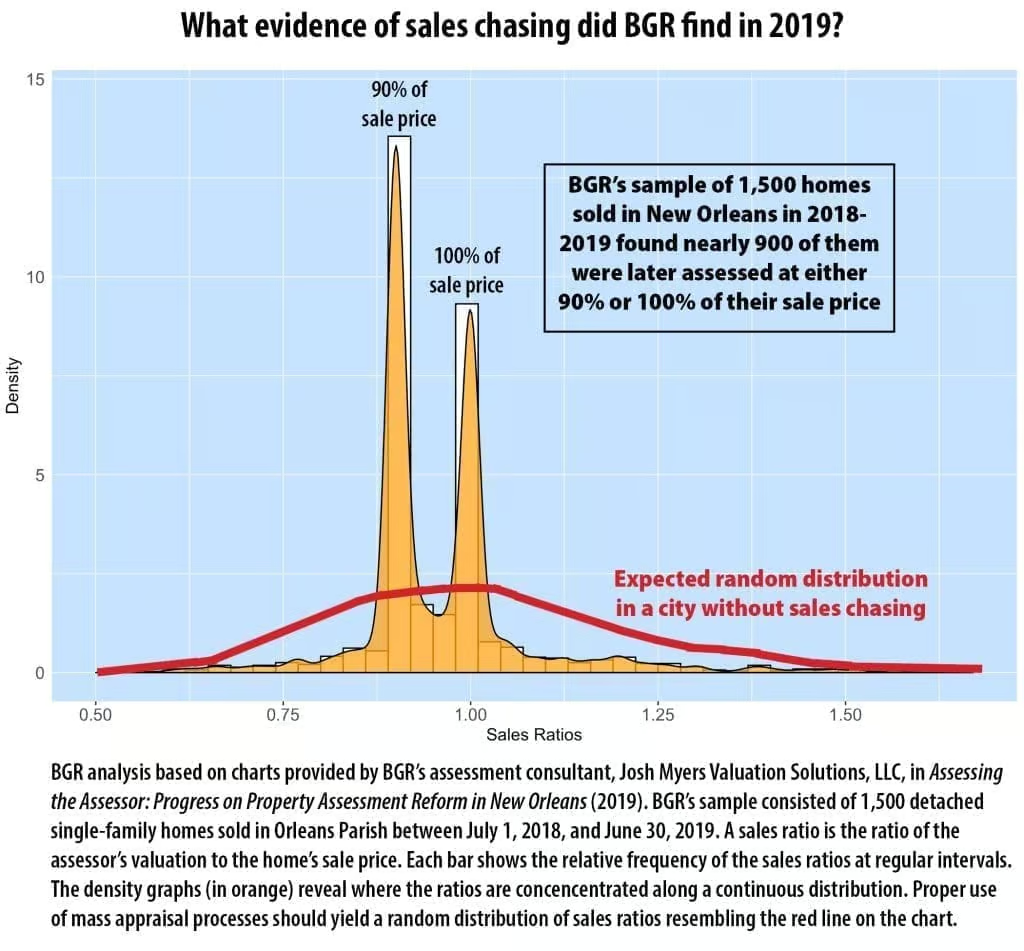

In addition, BGR found substantial evidence that the assessor frequently adjusts the valuations of recently sold properties to match or come to close to their sale price. An analysis of roughly 1,500 detached single-family homes sold between July 1, 2018 and June 30, 2019 showed that the assessor’s office adjusted the valuation of nearly 900 properties to reflect 90% or 100% of the sale price. As shown in the chart, the distribution of ratios shows dramatic peaks at 90% and 100%. An assessor cannot achieve this distribution through the consistent application of mass appraisal models. Rather, the dramatic peaks are achieved when an assessor selectively reappraises sold properties, a practice also known as “sales chasing.” Proper use of mass appraisal processes should yield a random distribution of sales ratios resembling the bell curve shape at the bottom of the chart.

Further, the office’s reliance on sale prices to value recently sold properties increased as the July 2019 deadline to mail next year’s assessment notices approached. And the sold properties were more likely to experience large increases in valuation from 2019 to 2020 than unsold residential properties, as shown in the chart.

Adjusting sold properties based solely on their sale price, a practice discouraged by national and State standards but widely used under the seven-assessor system, may seem logical. However, it undermines uniformity among property valuations. That is because the assessor uses sale prices to value sold properties and a different method to value unsold properties. This can create unfairness among taxpayers.

It also makes it difficult to evaluate the assessor’s true appraisal performance. For this report, BGR sought to conduct a commonly used study of the assessor’s appraisal performance for single-family homes in the recent reassessment. The study, which evaluates the assessor’s valuations against the sale prices for a sample of recently sold properties, can provide an effective measure of appraisal performance if an assessor uses the same method to value sold and unsold properties. However, with 60% of sampled properties valued based on their sale price, BGR could not complete its study. It would show an unusually high degree of appraisal accuracy and uniformity, and the findings would not accurately represent the broader population of New Orleans’ single-family homes because unsold properties cannot be valued in the same way (i.e., by sale price).

Further, BGR found that the assessor could not demonstrate that the office conducts annual studies to self-check the quality of its appraisal performance, as recommended by best practices. While the assessor told BGR that the office conducts the studies on a regular basis, the assessor did not produce a full copy of any previously conducted study. The assessor said that the office generally does not keep copies of any studies conducted in prior years. Assessment experts told BGR that, at a minimum, an assessor should keep copies of the studies during a reassessment cycle to justify and support changes to property valuations for the next cycle. The office’s current practices raise questions about quality assurance and public transparency.

Significant gaps also remain in the area of tax exemption administration. The assessor does not require nonprofit owners to reapply for the exemption annually, a practice that would help ensure that nonprofit-owned properties continue to meet eligibility requirements and comply with State law. Further, because exempt properties do not generate tax revenue, the assessor does not regularly revalue them. A regular revaluation of exempt properties would accurately inform policymakers and the public of the true cost of exemptions on the property tax base and tax revenue.

Finally, while BGR did not make a recommendation on funding the assessor’s office at the outset of the single assessor era, its subsequent reports have flagged the office’s surplus revenue. The assessor’s office receives a flat 2% fee on the total amount of property taxes billed in Orleans Parish each year. The fee is not based on the needs of the office, but rather grows as millage rates and property valuations increase. Over the years, the assessor’s fee has allowed the office to build a fund balance of $13.1 million, or 123% of its annual operating budget. The assessor has reserved $8 million of that amount for new office space, which he may pursue with the assistance of a special taxing district created this year by the State Legislature. The assessor’s substantial reserves call into question the size of the office’s dedicated funding, particularly at a time when the City of New Orleans and other property tax recipients are looking for additional revenue to address high-priority needs.

Overall, the report’s core finding is that the single assessor has put in place some of the necessary building blocks for a high-functioning assessment office but still falls short in crucial areas. The office’s valuation practices and lack of transparency raise serious concerns about the uniformity and fairness of property valuations in New Orleans, as well as the sufficiency of the processes that are supposed to inform them. Ongoing weaknesses in exemption administration further underscore that the job of reforming assessments in New Orleans is not done. Fortunately, that path to a fair and transparent assessment system remains clear and achievable, as this report’s recommendations indicate.