Conclusion

In looking to craft pension reforms, citizens and policymakers should keep in mind the vast gulf between public and private sector employees when it comes to retirement benefits. It is critical that reformers strive to provide public employee benefits that, as part of a total compensation package, will attract and retain high quality employees – while also ensuring that the level of benefits and their costs are fair to taxpayers.

Defined benefit pension plans for public employees in Louisiana as currently structured are in desperate need of reform. In most cases, the multipliers exceed the national median by wide margins, significantly increasing the rate at which employee benefits accrue and significantly reducing the amount of time that an employee needs to work in order to receive 100% of pre-retirement income.

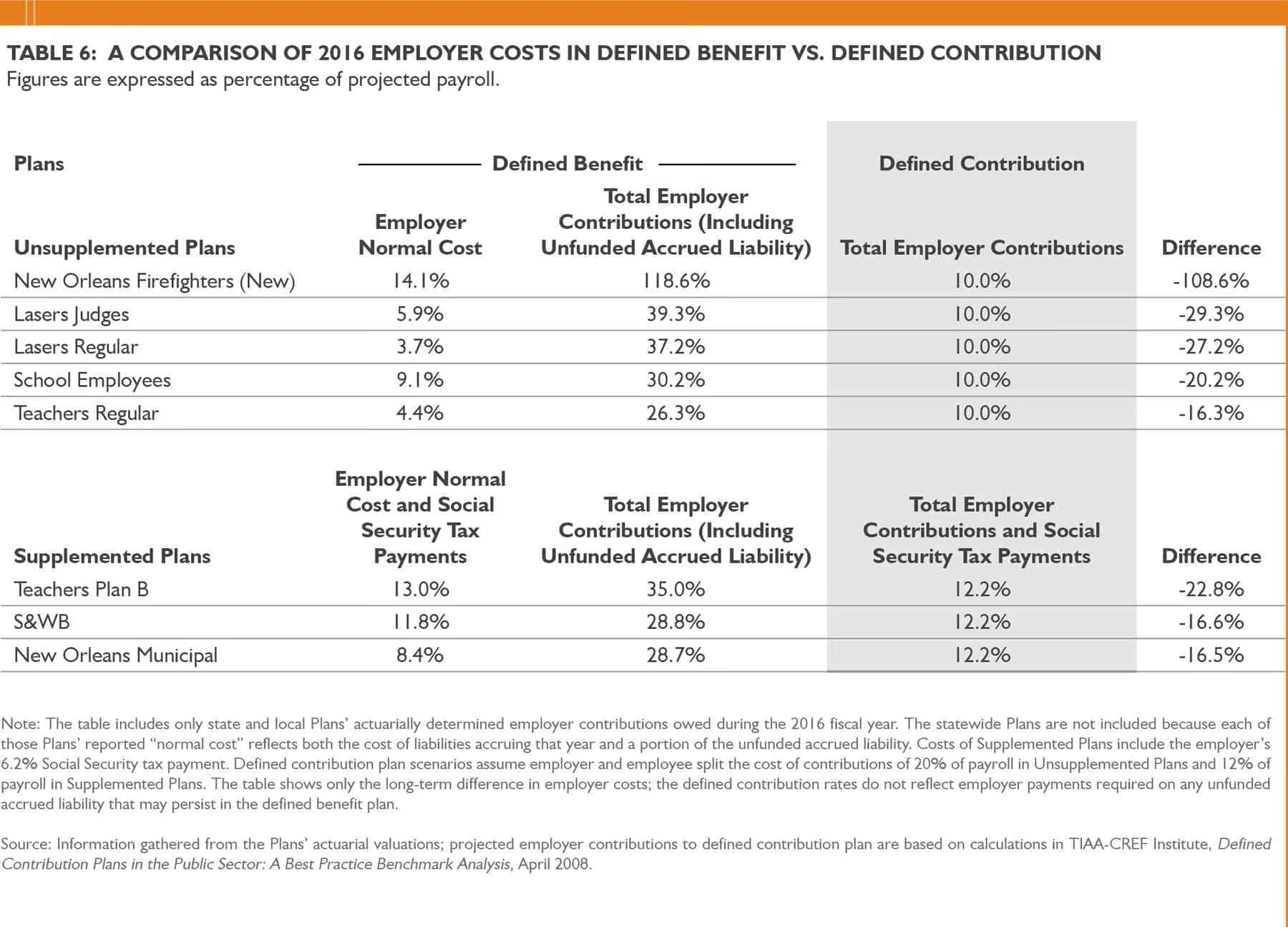

It remains true that the Plans in which local governments participate are more generous than national public sector medians in most respects. That generosity has contributed to ballooning costs – with employer contributions as high as 118% of total employee pay – threatening state and local government budgets. In other words, the cost of yesterday’s pension promises can diminish government’s ability to provide public services today and in the future.

Both public employees and private citizens alike bear the cost of past generations’ pension excesses. Policymakers ought to consider alternative pension plan designs that, in the long run, halt this generational cost transfer.

These plan designs would shift some, if not all, risk away from public employers. While employees take on additional risk, they also would enjoy greater plan portability. Under a defined contribution or cash balance plan, changing jobs would not mean having to start saving for retirement all over again. These plan designs may also better reflect the evolving expectations and career patterns of the work force.

At a minimum, policymakers should pursue reforms to the existing defined benefit offerings to bring them to a more reasonable level. That implies lowering multipliers to at least the national public sector median, raising the minimum retirement age, eliminating perks such as lump sum payment programs, limiting the income replacement to a need-based percentage of an employee’s salary, implementing a cap on benefits and leaving it to employees to self-fund cost of living adjustments.